A 793 credit score falls in the Very Good range, which covers credit scores from 740 to 799. You are comfortably above the national average FICO score of 714, and you have crossed the 740 line that most lenders use as the gateway to their best pricing.

At this level, the conversation changes. Approval is assumed. Rates are near the bottom of every lender's sheet. The work now is squeezing out the last pricing improvements where they exist, and protecting a credit score that took years to build.

The rest of this page covers what a 793 credit score gets you, where a few more points still pay, and the mistakes that cost people this tier.

Is 793 a Good Credit Score?

Yes. A 793 credit score is considered Very Good, which puts you above the national average of 714 and inside the pricing tier most lenders reserve their best offers for.

Credit scores run from 300 to 850, and lenders sort them into five ratings. Here is how the ranges break down and roughly what share of people falls into each.

| Credit Score | Credit Rating | % of Population |

|---|---|---|

| 300 – 579 | Poor | 16% |

| 580 – 669 | Fair | 17% |

| 670 – 739 | Good | 21% |

| 740 – 799 | Very Good | 25% |

| 800 – 850 | Exceptional | 21% |

Source: Experian, 2024 distribution (live rating table).

You have already passed 760 (Top-Tier Pricing) by 33 points. Lenders reserve their top-tier pricing for scores at 760 and up.

Your next milestones from here:

- +7 800 (Exceptional Floor): An 800 score reaches the Exceptional range and the best offers.

Credit Cards With a 793 Credit Score

Nearly every card on the market is available to you, including the premium travel and cash back cards with the strictest approval standards. Issuers compete for borrowers at this credit level, which means the signup bonuses and 0% intro offers you see advertised are realistic, not aspirational.

Two things still matter. First, approval odds are not 100% even here, because issuers also weigh income, existing accounts with them, and recent applications. Second, if you ever carry a balance, APR beats rewards. The average new card offer runs 23.79%, and even excellent credit prices only a few points below that.

The smart play at this level is selective applications for cards you will actually keep, since your long-standing accounts are part of what holds your credit score up.

Personal Loans With a 793 Credit Score

Personal loans price well for you. Borrowers above 720 average around 14.58% APR, and strong applicants at this credit level frequently beat that, especially at credit unions, where three-year loans average near 10.72%.

The main advice here is about purpose, not approval. At this credit level a personal loan makes sense for consolidating higher-rate debt or covering a planned expense at a fixed cost. Prequalify with soft pulls, take the best real offer, and keep the term as short as the payment allows.

See also: 8 Best Personal Loans for Good Credit

Mortgages With a 793 Credit Score

You are in the pricing tier mortgage lenders build their advertising around. Current data puts a 740 credit score near 6.75% on a 30-year conventional loan, 760 near 6.66%, and 780 and above near 6.59%.

Notice the shape of those numbers: the steps are getting smaller. The jump from 700 to 740 was worth real money. From 740 to 780, the gain shrinks to a fraction of a point. If your credit score sits at 740 to 759, reaching 760 before locking still buys a slightly better rate. Above 760, further improvement barely moves mortgage pricing at all.

What matters more at this level is everything else on the application. Debt-to-income ratio, down payment size, and loan type now influence your rate more than another 20 credit score points would.

See also: 10 Best Mortgage Lenders for Good Credit

Auto Loans With a 793 Credit Score

Auto lending treats you as a prime or super prime borrower. Super prime borrowers currently average 4.66% APR on new cars and 6.82% on used, per Experian data, and a 793 credit score puts you at or near those numbers.

Even here, the dealership finance office is a negotiation. Captive lenders sometimes offer promotional rates below market for well-qualified buyers, and those are worth taking. When no promotion applies, a credit union preapproval keeps the dealer honest.

The other lever is the term. At your rates, the interest penalty for a longer term is smaller than it is for lower credit tiers, but a 48 or 60 month term still beats 72 on total cost and keeps your equity position healthy.

See also: 10 Best Auto Loans

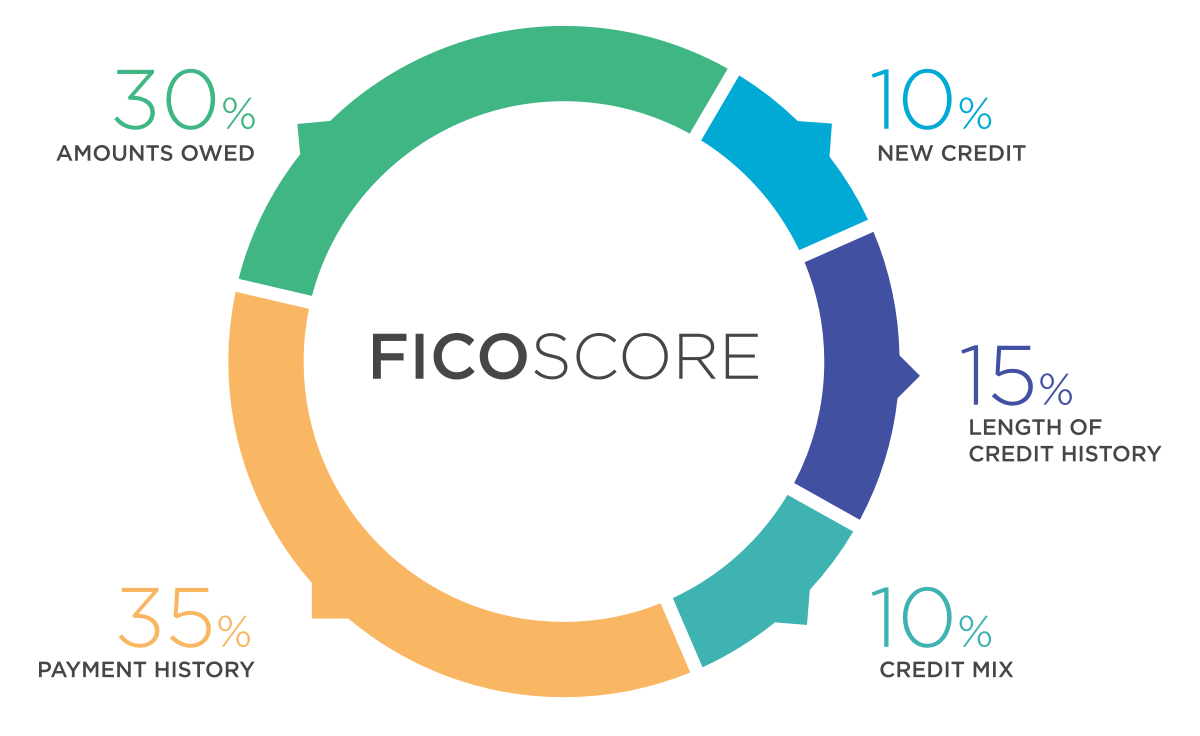

How Your FICO® Score Is Calculated

Your FICO® score is based on several key factors. Some have a much bigger impact than others, so focusing on the right habits can make a meaningful difference over time.

- Payment history (35%): Your history of on-time payments has the biggest impact on your FICO® score. Late payments, collections, and defaults can lower your credit scores quickly.

- Credit utilization (30%): This measures how much of your available credit you are using. Lower balances are generally better for your credit scores.

- Length of credit history (15%): Older credit accounts can help your credit profile. Lenders often prefer borrowers with a longer track record of responsible credit use.

- Credit mix (10%): Having different types of credit accounts, such as credit cards and installment loans, may help strengthen your credit profile.

- New credit inquiries (10%): Applying for several credit accounts within a short period can hurt your credit scores and may signal higher risk to lenders.

How to Protect a 793 Credit Score

At Very Good, maintenance beats improvement. The habits that keep you here:

1. Keep Credit Utilization in Single Digits

Reported balances under 10% of your limits are a signature of top-tier credit scores. If a large purchase spikes a statement balance, pay it down before the statement closes so the lower number reports.

2. Never Miss a Payment, Even a Small One

A single 30-day late payment can knock a Very Good credit score down by 80 points or more, because the cleaner the history, the harder the fall. Autopay on every account is non-negotiable insurance at this level.

3. Preserve Your Account Age

Your oldest accounts are load-bearing. Closing a long-held card shrinks your available credit and eventually shortens your average account age. Keep old cards open with a small recurring charge unless a fee makes that unreasonable.

4. Add New Credit Deliberately

You can absorb an occasional inquiry without real damage, but bursts of applications still register. Space applications out, and use soft-pull prequalification whenever a lender offers it.

5. Monitor for Errors and Fraud

At this credit level, the biggest threats are ones you did not cause: reporting errors and identity theft. Pull your free reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com a few times a year, and consider freezing your credit at all three bureaus when you are not actively applying.

What to Expect

From the 740s and 750s, crossing into the Exceptional range is a slow, steady drift rather than a project. Aging accounts and years of clean history do the work. There is no urgency, because almost nothing is priced better at 800 than at 780.

Credit scores at this level are stable by default. Protect the payment record, keep balances low, and the number takes care of itself.

Your Next Step

A 793 credit score already earns you the offers most people are working toward. The remaining opportunities are in the details: the right card, the right loan structure, the right timing.

Take the free Credit Comeback Quiz to get a personalized plan built around your credit situation and the best moves from here.

Jake is a personal finance writer with a background in consumer lending and credit counseling. He specializes in credit education, debt management, and helping readers understand the financial systems that affect their daily lives. His goal is simple: cut through the jargon and give people the information they actually need.