What a 417 Credit Score Means

A 417 credit score falls in the Poor range, which covers scores from 300 to 579. The national average FICO score is 714, so lenders will view your score as high risk.

Scores in this range usually come from serious negative marks. Late payments, charge-offs, collections, repossessions, and bankruptcy are the most common causes. A thin or empty credit file can also land here, since no credit history looks a lot like bad credit history to a lender.

A score under 500 puts you below the minimum for nearly every mainstream loan product, including FHA mortgages. Your first goal is simple: cross 500. That single threshold reopens the door to FHA financing and moves you out of the deepest pricing tier lenders use.

The rest of this page shows what lenders will actually offer at this score, with current rates, and the fastest ways to move up.

Where 417 Sits

Your next milestones from here:

- +83 500 (FHA Minimum): FHA mortgage eligibility begins at 500 with 10% down.

- +163 580 (FHA 3.5% Down): At 580 the FHA down payment requirement drops to 3.5%.

- +203 620 (Conventional Minimum): Most conventional mortgage lenders set their floor near 620.

Credit scores run from 300 to 850, and lenders sort them into five ratings. Here is how the ranges break down and roughly what share of people falls into each.

| Credit Score | Credit Rating | % of Population |

|---|---|---|

| 300 – 579 | Poor | 16% |

| 580 – 669 | Fair | 17% |

| 670 – 739 | Good | 21% |

| 740 – 799 | Very Good | 25% |

| 800 – 850 | Exceptional | 21% |

Source: Experian, 2024 distribution (live rating table).

Credit Cards With a 417 Credit Score

Secured credit cards are your most reliable option in the Poor range. You put down a refundable deposit, usually between $200 and $500, and that deposit becomes your credit limit. The card reports to the credit bureaus like any other card, so on-time payments build your score.

Many issuers review secured accounts after 6 to 12 months of on-time payments. Good behavior can earn back your deposit and an upgrade to an unsecured card.

Unsecured cards for bad credit exist, but read the terms closely. Many charge annual fees, monthly fees, and APRs near the top of the market. The average APR on new card offers is 23.79%, and cards in this range often exceed it. A secured card with no annual fee beats a fee-heavy unsecured card in almost every case.

See also: 8 Best Secured Credit Cards

Personal Loans With a 417 Credit Score

Approval odds for unsecured personal loans are low in the Poor range, and pricing is rough when approval happens. Borrowers below 690 commonly see APRs between 25% and 36%. Compare that to the 14.58% average for borrowers above 720, and the cost of a low score gets concrete.

Credit unions deserve a look before any online lender. Federal credit unions cannot charge more than 18% APR by law, which makes them the price ceiling worth knowing in this range.

Avoid payday loans and title loans completely. They do not build credit, and their fee structures are designed to keep you borrowing.

A credit builder loan is the better move at this score. The lender holds the loan amount in a savings account while you make payments, then releases the money to you at the end. Payments report to the bureaus, so you build history without needing approval based on your current score.

See also: 9 Best Personal Loans for Bad Credit

Mortgages With a 417 Credit Score

Conventional and FHA lenders will decline applications at this score. FHA requires a minimum of 500, and conventional lenders typically want 620 or higher. Focus on the credit rebuilding steps below before applying, since every application adds a hard inquiry.

Rate pricing makes the case for waiting when you can. The gap between a 620 borrower and a 760 borrower runs about 1.5 to 1.8 percentage points, worth more than $56,000 in interest on a $300,000 loan.

See also: 8 Best Mortgage Loans for Bad Credit

Auto Loans With a 417 Credit Score

This is where a Poor score costs the most, because approval is actually common. Lenders in the deep subprime tier approve these loans and price them accordingly.

Deep subprime borrowers currently average 16.01% APR on new car loans and 21.58% on used, per Experian data. Super prime borrowers pay 4.66% on new. On a $30,000 loan over 60 months, that gap costs roughly $219 more per month and over $13,000 in extra interest.

If you need a car now, three moves limit the damage. Buy less car than the lender approves you for. Get a preapproval from a credit union before you visit a dealership. Refinance after 12 to 18 months of on-time payments, once your score has moved into a better tier.

See also: 7 Best Auto Loans for Bad Credit

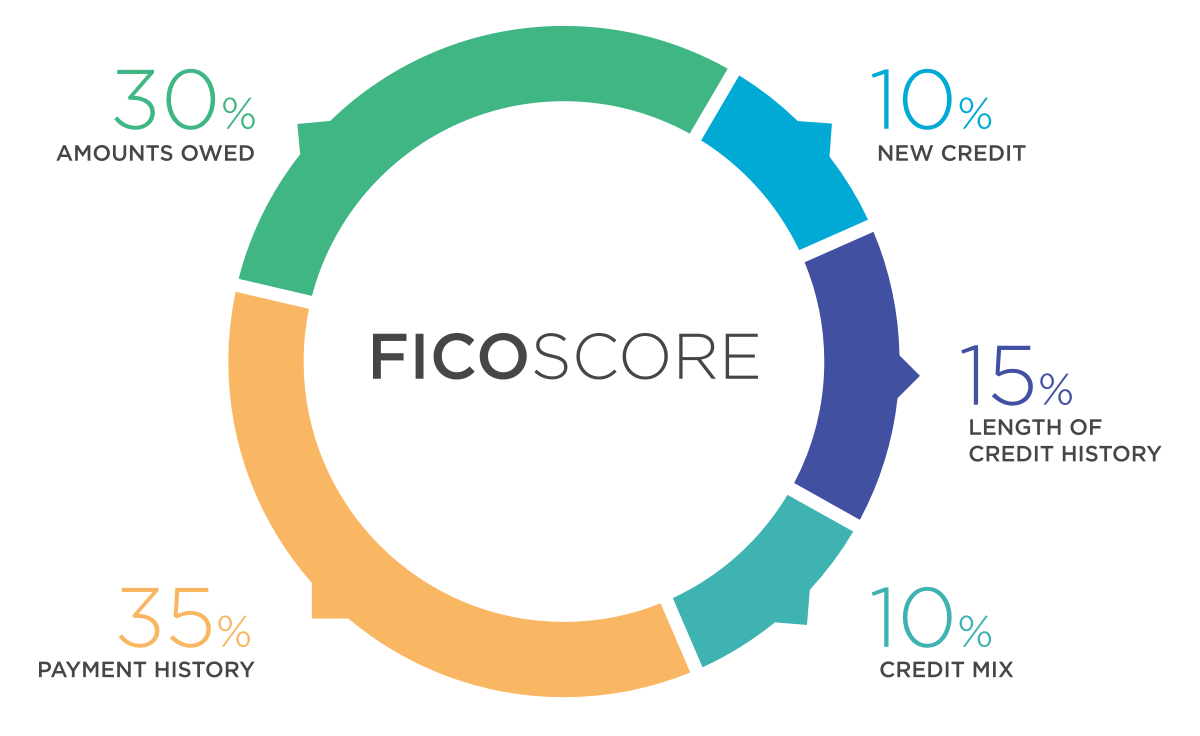

How Your FICO® Score Is Calculated

Your FICO® score is based on several key factors. Some have a much bigger impact than others, so focusing on the right habits can make a meaningful difference over time.

- Payment history (35%): Your history of on-time payments has the biggest impact on your FICO® score. Late payments, collections, and defaults can lower your credit scores quickly.

- Credit utilization (30%): This measures how much of your available credit you are using. Lower balances are generally better for your credit scores.

- Length of credit history (15%): Older credit accounts can help your credit profile. Lenders often prefer borrowers with a longer track record of responsible credit use.

- Credit mix (10%): Having different types of credit accounts, such as credit cards and installment loans, may help strengthen your credit profile.

- New credit inquiries (10%): Applying for several credit accounts within a short period can hurt your credit scores and may signal higher risk to lenders.

How to Improve a 417 Credit Score

The Poor range responds faster to good behavior than any other band, because there is more room to move. Here is the order of operations:

1. Pull All Three Credit Reports and Dispute Errors

Get your free reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Look for accounts you do not recognize, incorrect balances, and late payments you actually made on time. Disputes are free and the bureaus must respond within 30 days.

If your report has negative items that are accurate but questionable, credit repair companies can handle disputes on your behalf. That includes late payments, collections, charge-offs, and judgments.

2. Open a Credit Builder Loan

No credit check, low monthly cost, and every payment reports to the bureaus. This is the cheapest way to add positive installment history at this score.

See also: 8 Best Credit Builder Loans

3. Add a Secured Card and Keep Utilization Low

The deposit removes the approval problem. Use the card for one small recurring bill, pay it in full monthly, and keep the balance under 10% of your limit. Payment history and utilization together drive 65% of your FICO score.

4. Become an Authorized User

If someone close to you has an old account with perfect payment history and low utilization, ask to be added as an authorized user. Their account history lands on your report, often within a month or two.

5. Report Your Rent Payments

Rent reporting services add your rent history to your credit file for a small fee. It is one of the few ways to get credit for a bill you already pay.

What to Expect

From under 500, six months of clean payment history plus a credit builder loan and secured card can realistically move you 50 to 100 points. The exact pace depends on what is dragging your score down, since recent late payments fade slower than old ones.

Scores are not permanent. Every negative item on your report has an expiration date, and positive history starts working for you the first month it reports.

Your Next Step

A 417 credit score is a starting point, not a verdict. The fastest movers in the Poor range are people who stop new damage, add one or two positive accounts, and let the months stack up.

Take the free Credit Comeback Quiz to get a personalized plan built around your credit situation and the fastest steps forward.

Jake is a personal finance writer with a background in consumer lending and credit counseling. He specializes in credit education, debt management, and helping readers understand the financial systems that affect their daily lives. His goal is simple: cut through the jargon and give people the information they actually need.