A 723 credit score falls in the Good range, which covers credit scores from 670 to 739. Lenders treat this range as acceptable risk, so approvals come easily for most credit cards, auto loans, and mortgages.

What changes inside this range is price. A Good credit score qualifies you for mainstream products, but the best advertised rates are usually reserved for scores of 740 and up. That gap is where your money goes.

You have crossed 700, which many lenders use as an informal tier break. Your remaining target is 740, 17 points away, where top-tier mortgage pricing and premium card approvals open up.

The rest of this page shows what lenders offer at this credit score, where the better pricing starts, and how to close the gap.

Is 723 a Good Credit Score?

Yes. A 723 credit score falls in the Good range, which covers 670 to 739 and includes the largest share of American borrowers.

Credit scores run from 300 to 850, and lenders sort them into five ratings. Here is how the ranges break down and roughly what share of people falls into each.

| Credit Score | Credit Rating | % of Population |

|---|---|---|

| 300 – 579 | Poor | 16% |

| 580 – 669 | Fair | 17% |

| 670 – 739 | Good | 21% |

| 740 – 799 | Very Good | 25% |

| 800 – 850 | Exceptional | 21% |

Source: Experian, 2024 distribution (live rating table).

You have already passed 700 (Strong Approvals) by 23 points. A 700 score opens broad approvals and noticeably better rates.

Your next milestones from here:

- +17 740 (Very Good Floor): At 740 you reach the best mainstream mortgage pricing tier.

- +37 760 (Top-Tier Pricing): Lenders reserve their top-tier pricing for scores at 760 and up.

- +77 800 (Exceptional Floor): An 800 score reaches the Exceptional range and the best offers.

Credit Cards With a 723 Credit Score

The Good range unlocks the cards most people actually want. Cash back cards, travel cards, and 0% intro APR offers all approve regularly at this credit level. Premium cards with high annual fees and top-tier rewards get pickier, and many of those approvals concentrate above 740.

Pricing still matters. The average APR on new card offers is 23.79%, and a Good credit score typically lands somewhat below that average but not at the floor. If you carry a balance, the APR matters more than any rewards program, so weigh that first.

The biggest card mistake in this range is over-applying. Your credit score is close enough to Very Good that a burst of hard inquiries can push the better offers out of reach right before you cross.

Personal Loans With a 723 Credit Score

Personal loan pricing improves meaningfully in the Good range. Borrowers between 690 and 719 average around 19.04% APR, and borrowers above 720 average 14.58%. If your credit score sits near either line, a small improvement before applying has a direct dollar payoff.

Credit unions still tend to beat online lenders here, with three-year loans averaging near 10.72%. Prequalify with two or three lenders through soft pulls, compare real offers, and only submit a full application to the winner.

See also: 8 Best Personal Loans for Good Credit

Mortgages With a 723 Credit Score

Approval is not the question at a 723 credit score. Every mainstream mortgage type is available, conventional, FHA, VA, and jumbo at the higher end of the range. The question is the rate sheet.

Mortgage pricing steps up in tiers. Current data puts a 700 credit score at roughly 6.91% on a 30-year conventional loan, while 740 prices near 6.75% and 760 near 6.66%. Those look like small gaps, but on a $300,000 loan, moving from the high 600s to 740 is worth roughly $83 a month and about $29,000 over the life of the loan.

If a home purchase is 6 to 12 months out, that math should drive your plan. Keep balances low, add no new accounts, and let your credit score climb into the next pricing tier before you lock a rate.

See also: 10 Best Mortgage Lenders for Good Credit

Auto Loans With a 723 Credit Score

A Good credit score puts you in prime territory for auto lending. Prime borrowers currently average around 6.4% APR on new cars and 9.06% on used, per Experian data. That is a different world from the double-digit rates below 660.

Dealers know most Good-credit buyers do not shop their financing, and that is where the margin hides. Walk in with a preapproval from a bank or credit union, and let the dealer try to beat it. When they can, take it. When they cannot, you already have your loan.

Watch the term length too. Stretching to 72 or 84 months lowers the payment but raises the total cost sharply, and it keeps you underwater on the vehicle longer.

See also: 10 Best Auto Loans

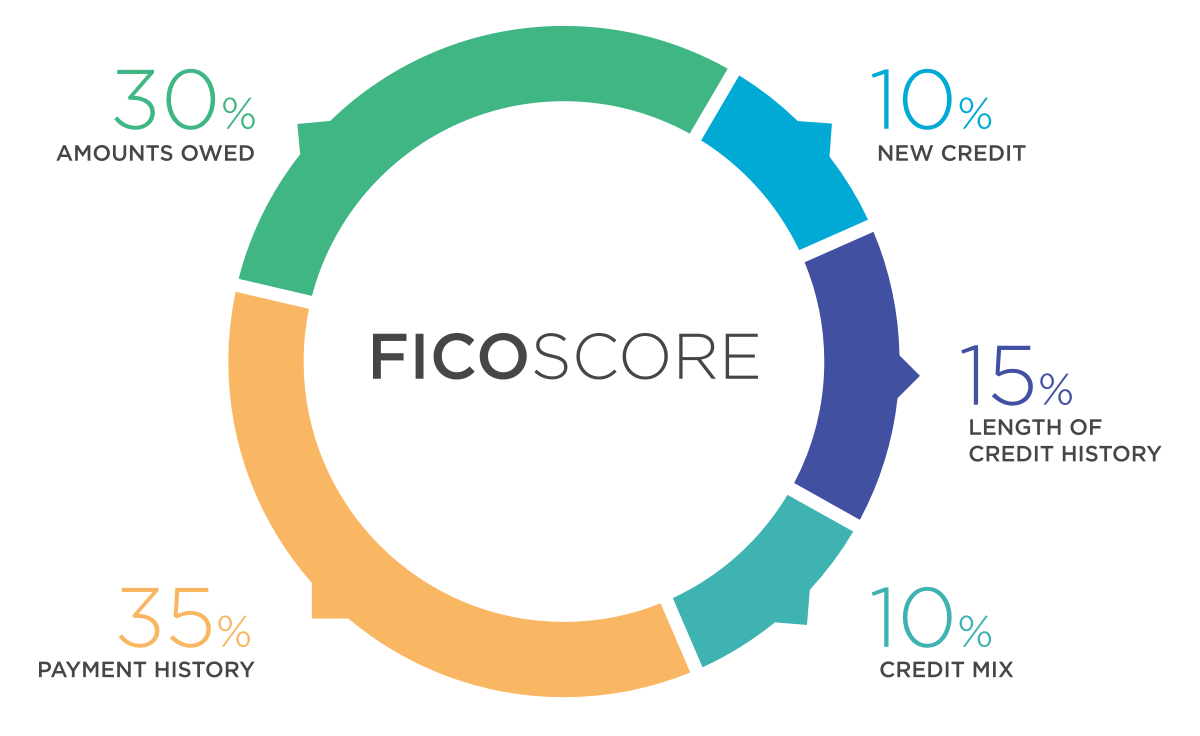

How Your FICO® Score Is Calculated

Your FICO® score is based on several key factors. Some have a much bigger impact than others, so focusing on the right habits can make a meaningful difference over time.

- Payment history (35%): Your history of on-time payments has the biggest impact on your FICO® score. Late payments, collections, and defaults can lower your credit scores quickly.

- Credit utilization (30%): This measures how much of your available credit you are using. Lower balances are generally better for your credit scores.

- Length of credit history (15%): Older credit accounts can help your credit profile. Lenders often prefer borrowers with a longer track record of responsible credit use.

- Credit mix (10%): Having different types of credit accounts, such as credit cards and installment loans, may help strengthen your credit profile.

- New credit inquiries (10%): Applying for several credit accounts within a short period can hurt your credit scores and may signal higher risk to lenders.

How to Improve a 723 Credit Score

At this level, improvement is about precision, not repair. The moves that push a Good credit score into Very Good:

1. Push Credit Utilization Under 10%

Under 30% is fine. Under 10% is where top-tier credit scores live. If you pay in full monthly but your reported balance is high, pay the card down before the statement closes, since the statement balance is usually what gets reported.

2. Keep Your Payment Record Spotless

One late payment costs a Good credit score dearly, precisely because your history is clean. Autopay on every account, at least for the minimum, removes the risk entirely. Payment history and credit utilization together drive 65% of your FICO score.

3. Let Your Accounts Age

Length of credit history makes up 15% of your FICO score, and there is no shortcut for it. Keep your oldest cards open with a small recurring charge, and think twice before closing anything.

4. Be Strategic About New Credit

Every hard inquiry matters more when you are close to a tier line. If you are within 20 points of 700 or 740, hold new applications until you cross. When you do rate-shop a mortgage or auto loan, keep it inside a 14 to 45 day window so it counts as one inquiry.

5. Check All Three Reports for Errors

Pull your free reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. At this credit level, errors are the most common thing standing between you and the next tier. Disputes are free and the bureaus must respond within 30 days.

What to Expect

From the low 700s, reaching 740 is mostly about patience and discipline. Keep utilization in single digits, add nothing negative, and let your accounts age. Most people in your position cross within a year without doing anything dramatic.

Credit scores reward consistency above everything. The habits that got you to Good are the same ones that finish the climb.

Your Next Step

A 723 credit score means you have already built something worth protecting. The remaining gap between Good and the best pricing tiers is small, and closing it is mostly maintenance.

Take the free Credit Comeback Quiz to get a personalized plan built around your credit situation and the fastest steps forward.

Jake is a personal finance writer with a background in consumer lending and credit counseling. He specializes in credit education, debt management, and helping readers understand the financial systems that affect their daily lives. His goal is simple: cut through the jargon and give people the information they actually need.