Filing for bankruptcy can feel like hitting rock bottom—but it doesn’t mean your credit is ruined forever. While most people think they have to wait seven to ten years for it to fall off their credit report, there are ways to challenge it and potentially remove it early.

Even if it stays, there’s a lot you can do right now to speed up your credit recovery. This guide breaks down how to dispute a bankruptcy, when it works, and what steps you can take to rebuild your credit faster.

Not sure where to start with your credit?

Answer a few simple questions and get a free step-by-step plan to rebuild your credit.

How long does a bankruptcy stay on your credit report?

The amount of time a bankruptcy stays on your credit report depends on which type you filed:

- Chapter 7 bankruptcy stays for 10 years from the date you filed.

- Chapter 13 bankruptcy stays for 7 years from the filing date.

A common mistake people make is assuming the countdown starts when the bankruptcy is discharged. It doesn’t. The clock starts the day you file, no matter how long the court process takes.

Also, keep in mind that even after the bankruptcy falls off your credit report, the accounts included in the filing may stick around longer—unless you take steps to dispute those, too.

How Removing a Bankruptcy Works—and Why It’s Possible

Most people think you just have to wait it out—but in some cases, you can get a bankruptcy removed early if it wasn’t properly verified.

Credit bureaus are required under the Fair Credit Reporting Act (FCRA) to report only information that’s accurate and verifiable. That includes public records like bankruptcies. But here’s the catch: credit bureaus don’t get bankruptcy info directly from the courts. They typically pull it from third-party sources.

That creates room for error—and opportunity.

If you send a procedural request letter asking the credit bureau how they verified the bankruptcy, they may claim they confirmed it with the court. But most courts don’t verify anything with credit bureaus. If you can get written confirmation from the court that they don’t verify records, you can send that back to the bureau and request removal.

It’s not a guaranteed fix, but it’s a legitimate path that’s worked for many people.

Step-by-Step: How to Dispute a Bankruptcy on Your Credit Report

If you’re trying to get a bankruptcy removed from your credit report early, this is the process to follow. It’s not guaranteed to work, but it’s legal, free to try on your own, and has worked for others.

1. Get Your Credit Reports

Start by pulling your credit reports from all three major credit bureaus: Equifax, Experian, and TransUnion.

You can get them for free at AnnualCreditReport.com. You’re entitled to one free report from each bureau every 12 months, but during certain periods (like post-COVID extensions), you may be able to get them more frequently.

Make sure you check all three reports—bankruptcies don’t always show up the same way across bureaus.

2. Check for Errors or Inconsistencies

Go through the bankruptcy section line by line. Look for anything that could be incorrect or unverifiable:

- Your name or address is misspelled

- The filing date is wrong

- The case number is missing or incorrect

- It says “dismissed” when it was discharged—or vice versa

- Different bureaus list different dates or statuses

- The same bankruptcy is listed twice under different case numbers

Even a small discrepancy could be grounds for removal.

3. Send a Procedural Request Letter to Each Bureau

Next, send a letter to each credit bureau asking how they verified the bankruptcy. This is known as a procedural request under the Fair Credit Reporting Act.

Here’s the key: credit bureaus often say they verified the information “with the court,” but most courts don’t communicate with credit bureaus directly.

This opens the door for removal if the bureau can’t properly verify the record.

What to include in the letter:

- Your name and contact information

- A clear reference to the bankruptcy listing

- A statement requesting the method of verification

- A copy of your credit report showing the listing (optional but helpful)

- A request to remove the bankruptcy if they cannot verify it

Tip: Keep your letter short and factual. Don’t admit to the bankruptcy or give extra details.

4. Contact the Court Directly

While you’re waiting for responses from the credit bureaus, contact the court where your bankruptcy was filed.

Ask:

“Does your court verify bankruptcy records with credit reporting agencies?”

They’ll usually say no—and if you can, get that answer in writing.

This written response can be used as evidence in your next round of disputes.

5. Send Follow-Up Dispute With New Evidence

If the court confirms they don’t verify bankruptcy data, send that statement back to the credit bureaus along with a follow-up letter.

In this letter:

- Reiterate your dispute

- Reference their earlier claim of verification

- Include the court’s written statement

- Request deletion based on lack of verifiable source

You’re not arguing that the bankruptcy didn’t happen—you’re arguing that it was not properly verified.

6. Track Your Disputes and Results

Credit bureaus have 30 days to investigate and respond to your dispute.

- Keep a copy of every letter you send

- Send everything via certified mail with return receipt

- Save any responses you receive from the bureaus or the court

- If they delete the bankruptcy, monitor your credit reports to make sure it doesn’t get reinserted

If it is reinserted, the bureau must notify you in writing within five business days. You can dispute it again or file a complaint with the CFPB.

What about the accounts included in bankruptcy?

Removing the bankruptcy itself is one thing, but you’ll also want to review the individual accounts that were part of the filing.

These accounts usually show up with remarks like “included in bankruptcy,” “charged off,” or “closed by grantor.” Here’s what to know:

- Each account has its own reporting timeline. Even if the bankruptcy stays for 7–10 years, individual accounts might fall off sooner (typically 7 years from the original delinquency date).

- You can dispute these accounts separately. If the balances are incorrect, if they’re listed multiple times, or if they show the wrong status, dispute them directly.

- Don’t assume the accounts are accurate. Creditors and bureaus often make errors when reporting accounts after a bankruptcy, especially with older records.

Removing these secondary negative items can improve your credit score—even if the bankruptcy remains.

How Bankruptcy Affects Your Credit Score

Bankruptcy has one of the biggest impacts of any negative item on your credit report—but the effect depends on where your credit score was to begin with.

According to FICO:

- If your credit score was around 680, a bankruptcy might drop it by 130–150 points

- If your score was closer to 780, the drop could be 220–240 points

The higher your score, the harder the fall.

That said, your score doesn’t stay in the basement forever. Most people see their credit scores start to improve within 12–24 months—especially if they build positive history and avoid new derogatory marks.

Removing a bankruptcy early can speed this up significantly. In some cases, people see their scores jump 100+ points just from deleting the bankruptcy—even if everything else stays the same.

What if the bankruptcy isn’t removed?

Not every dispute leads to removal on the first try. That doesn’t mean you’re out of options.

Send a Follow-Up Dispute

If the credit bureau responds that your bankruptcy was “verified,” don’t stop there. You can send a second dispute—especially if you now have additional documentation from the court stating they don’t verify records for credit bureaus.

Include:

- A copy of your original letter

- The bureau’s response

- Any new evidence or clarification

- A firm request for deletion based on lack of verification

Space out follow-up disputes by 30–45 days to avoid being flagged as frivolous.

Escalate the Issue

If your disputes keep getting rejected, escalate the situation:

- File a complaint with the CFPB (Consumer Financial Protection Bureau)

- Include copies of your letters and the court’s statement

- Explain why you believe the bureau failed to verify the information properly

- Submit a reinvestigation request

- Under the FCRA, you have the right to challenge the accuracy and verification process at any time

These steps don’t guarantee removal, but they show the credit bureaus you’re not going away quietly.

How to Rebuild Your Credit After Bankruptcy

Whether your bankruptcy gets removed or not, rebuilding your credit should start immediately.

Here’s what to focus on:

- Pay all bills on time—no exceptions. Payment history is the biggest factor in your credit score. Even one late payment can set you back.

- Use a secured credit card or credit builder loan. These tools help rebuild positive history when used responsibly.

- Avoid new debt unless absolutely necessary. Focus on managing what you have—not adding to it.

- Consider tools that report more data.

- Experian Boost can add utility and phone payments to your credit file

- Services like RentReporters or LevelCredit can report on-time rent payments

- Monitor your credit monthly. Use free tools or apps to track your score and make sure new errors don’t show up

Rebuilding doesn’t happen overnight—but steady habits can move your score in the right direction much faster than you might think.

Should you use a credit repair company?

Credit repair companies aren’t for everyone, but if the dispute process feels confusing or time-consuming, they can take the pressure off and handle it for you.

Pros:

- They handle the dispute process for you

- Familiar with what language and strategies work best

- May be more persistent with multiple dispute rounds

Cons:

- Not free—typically $50 to $130 per month

- Some companies overpromise or use shady tactics

- Results aren’t guaranteed

What to Look For:

- Clear pricing and refund policy

- No upfront fees

- Strong customer reviews

- Specialization in public record disputes (like bankruptcy)

- Willingness to explain their process before you sign up

We’ve reviewed and ranked top credit repair services to help you compare options.

Final Thoughts

A bankruptcy on your credit report can feel like a dead end—but it doesn’t have to be.

You may be able to get it removed early by challenging how it was verified. And even if it stays, you’re not stuck. With the right strategy, you can rebuild your credit, qualify for better rates, and move forward with confidence.

Take the next step—because your financial future isn’t defined by your past.

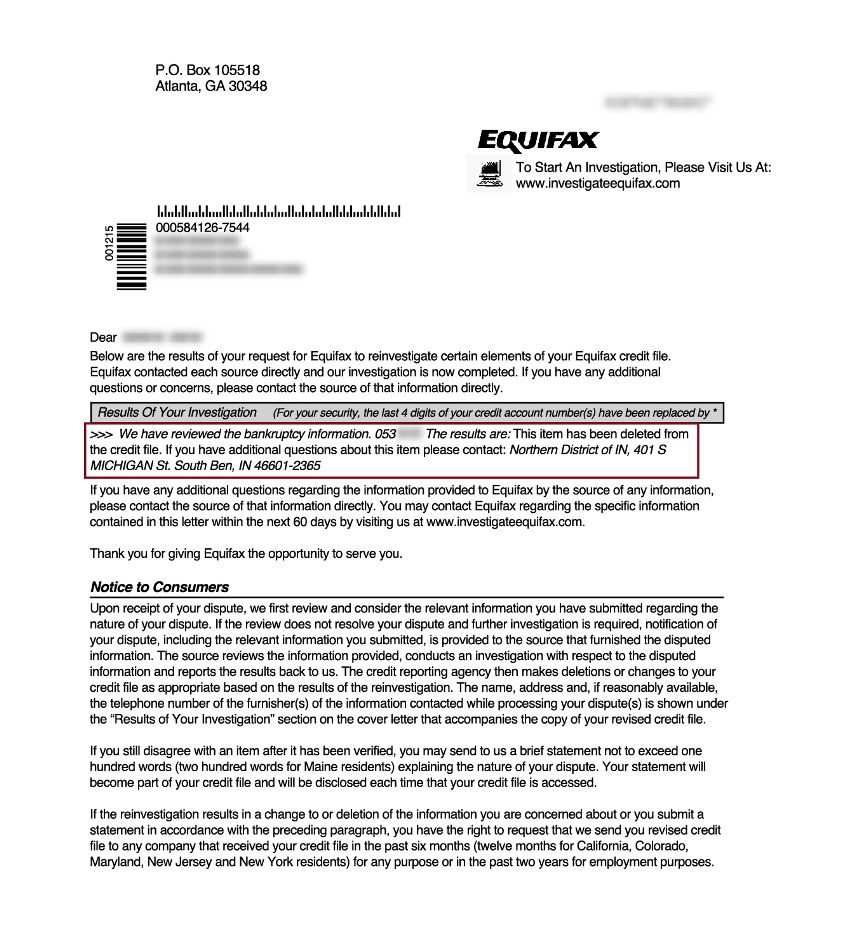

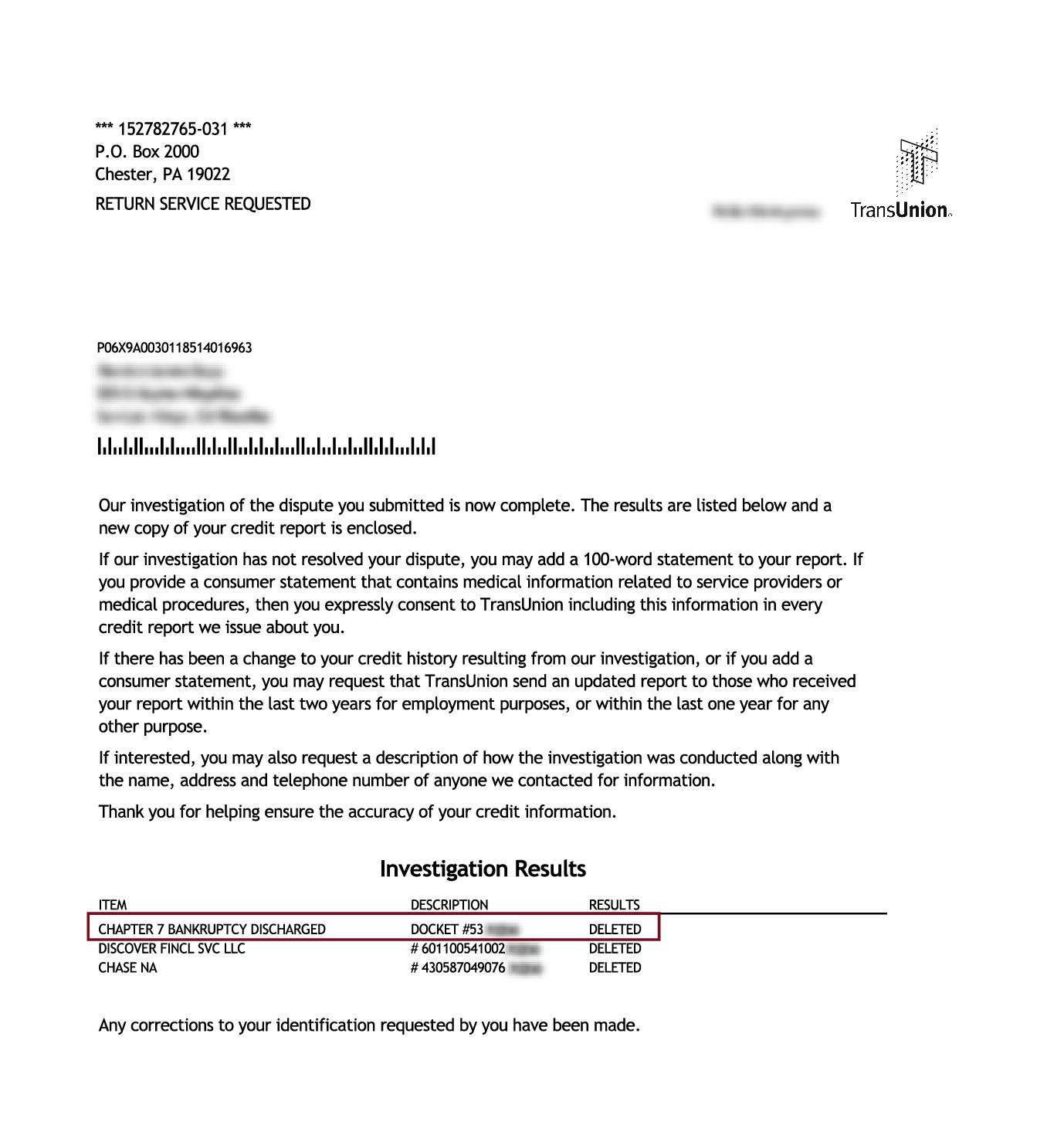

Chapter 7 Bankruptcies Removed

These images are from actual credit reports after a successful dispute. Results are not guaranteed and may vary.